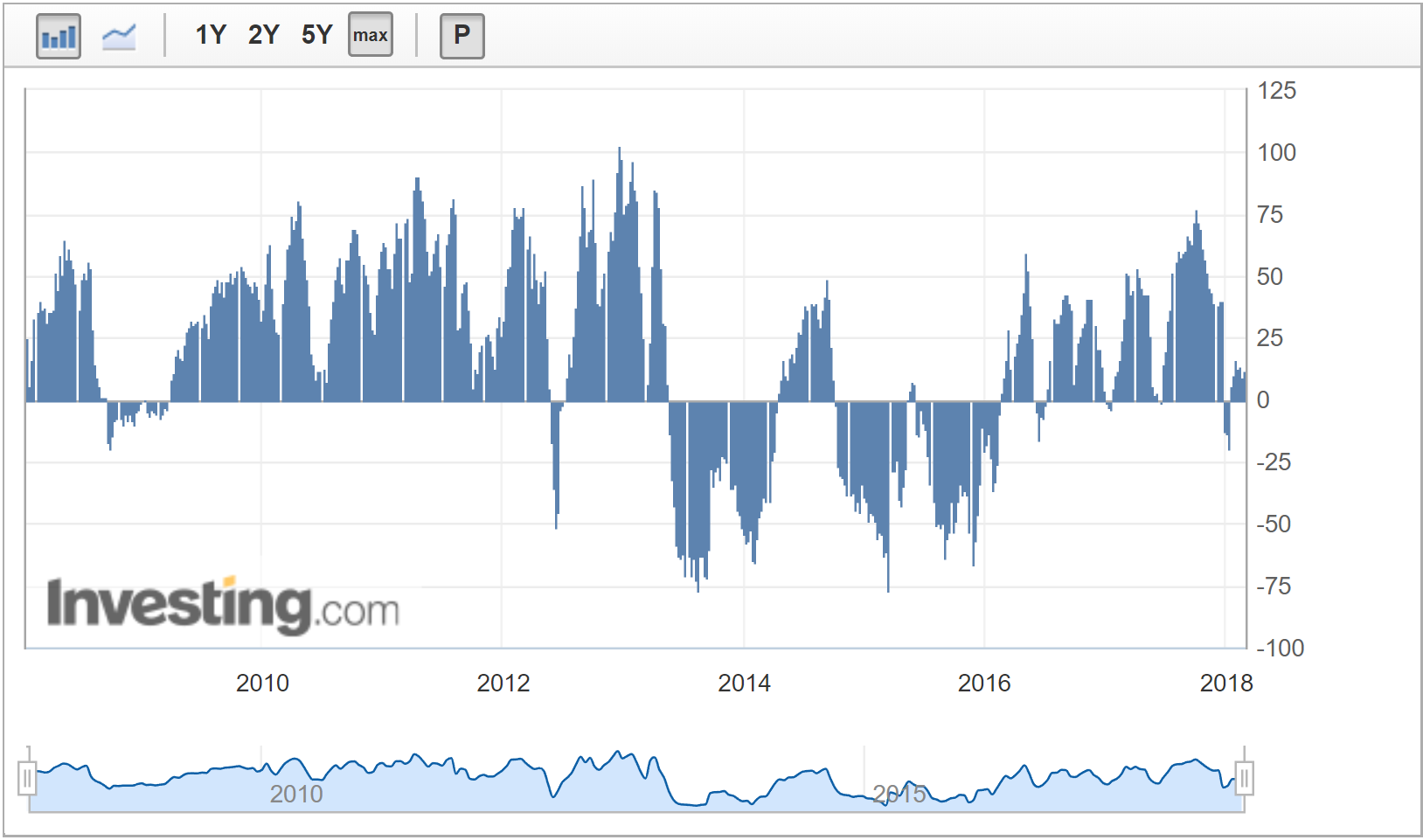

Speculative positioning remains modestly bullish at 12k contracts:

Advertisement

Gold was soft:

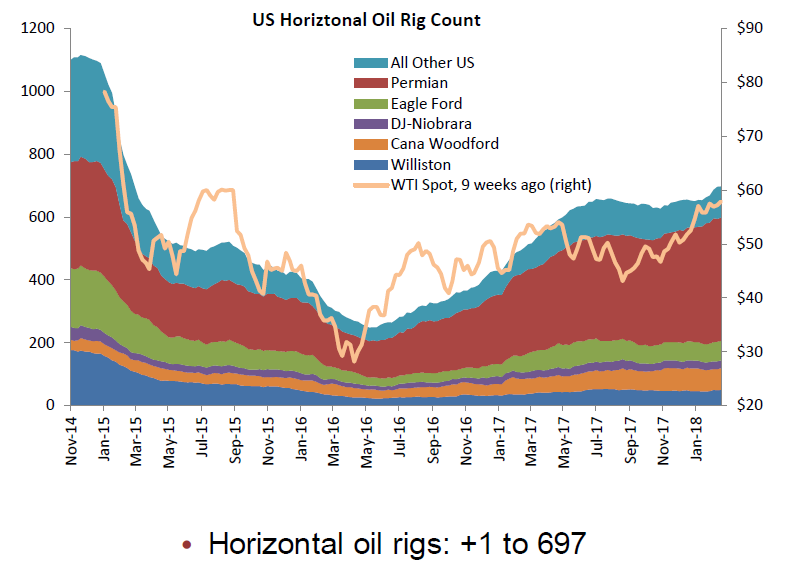

Oil strong:

As the US rig count rose only three to 978:

Advertisement

• Total US oil rigs took an anticipated breather this week, +1 to 799

• Horizontal oil rigs were up, +1 to 697

• The oil price continues to recover

• If rig count additions continue on our forecast trajectory, expect this to weigh on sentiment during March, particularly if supply gains surprise to the upside

Base metals fell:

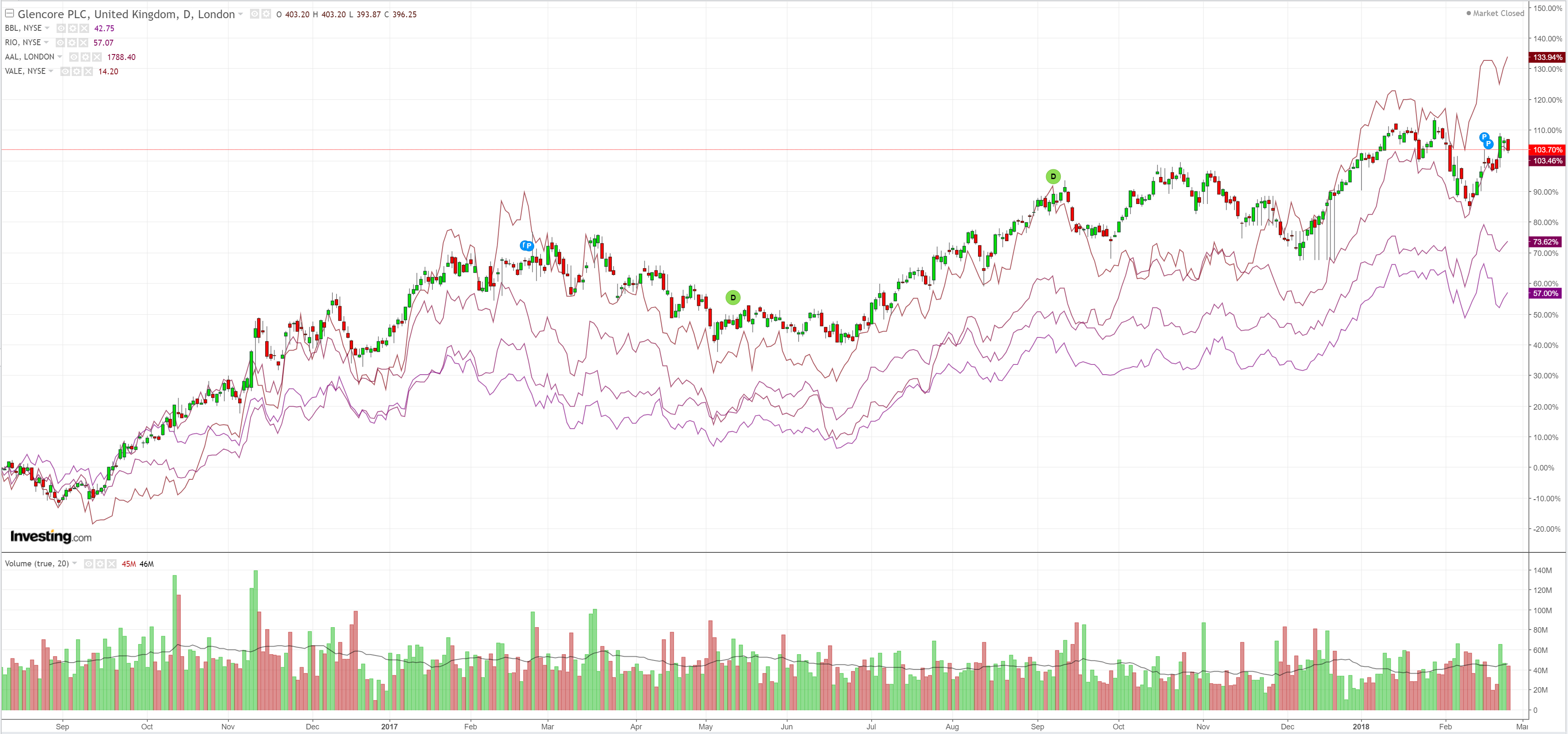

Big miners lifted:

Advertisement

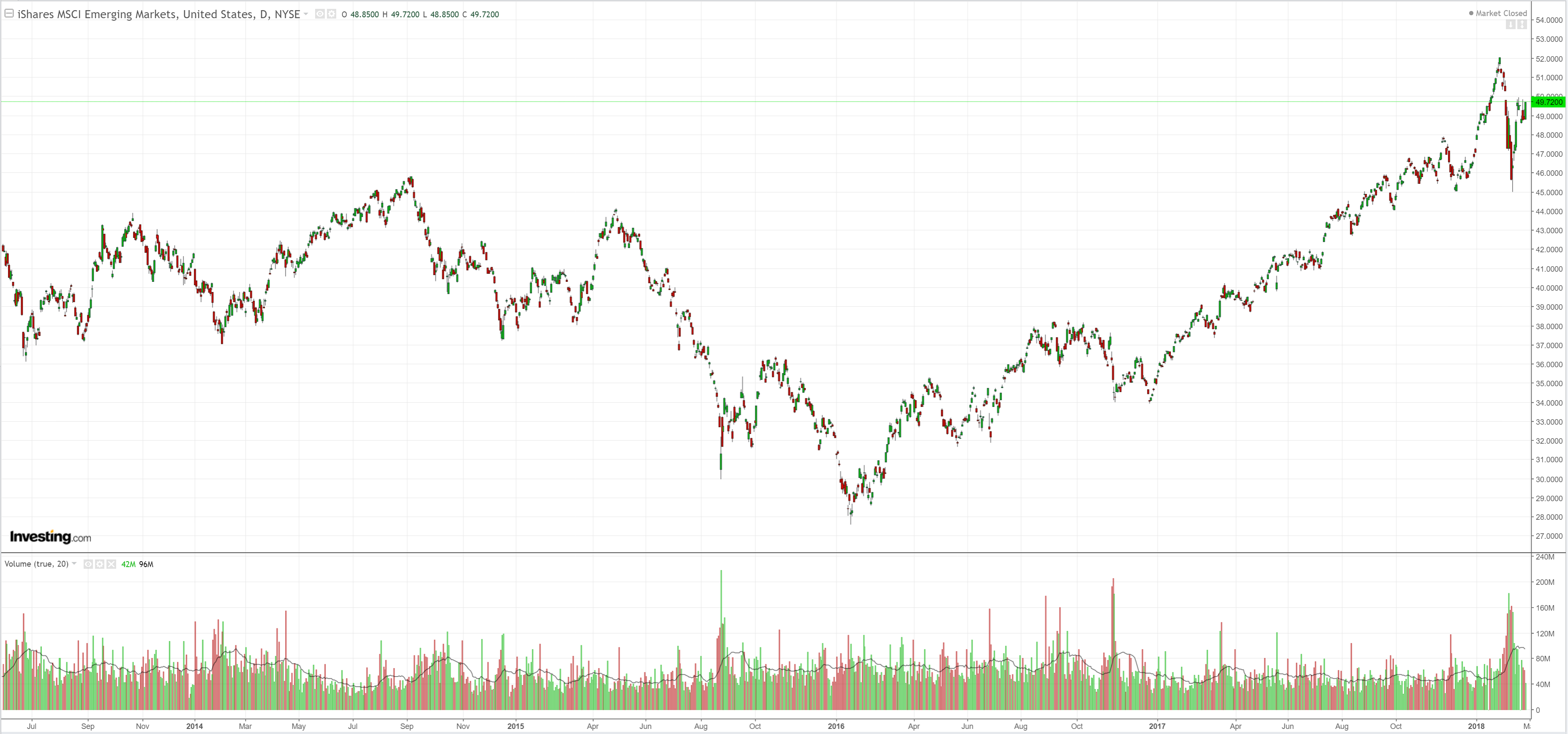

EM stocks bounced despite DXY:

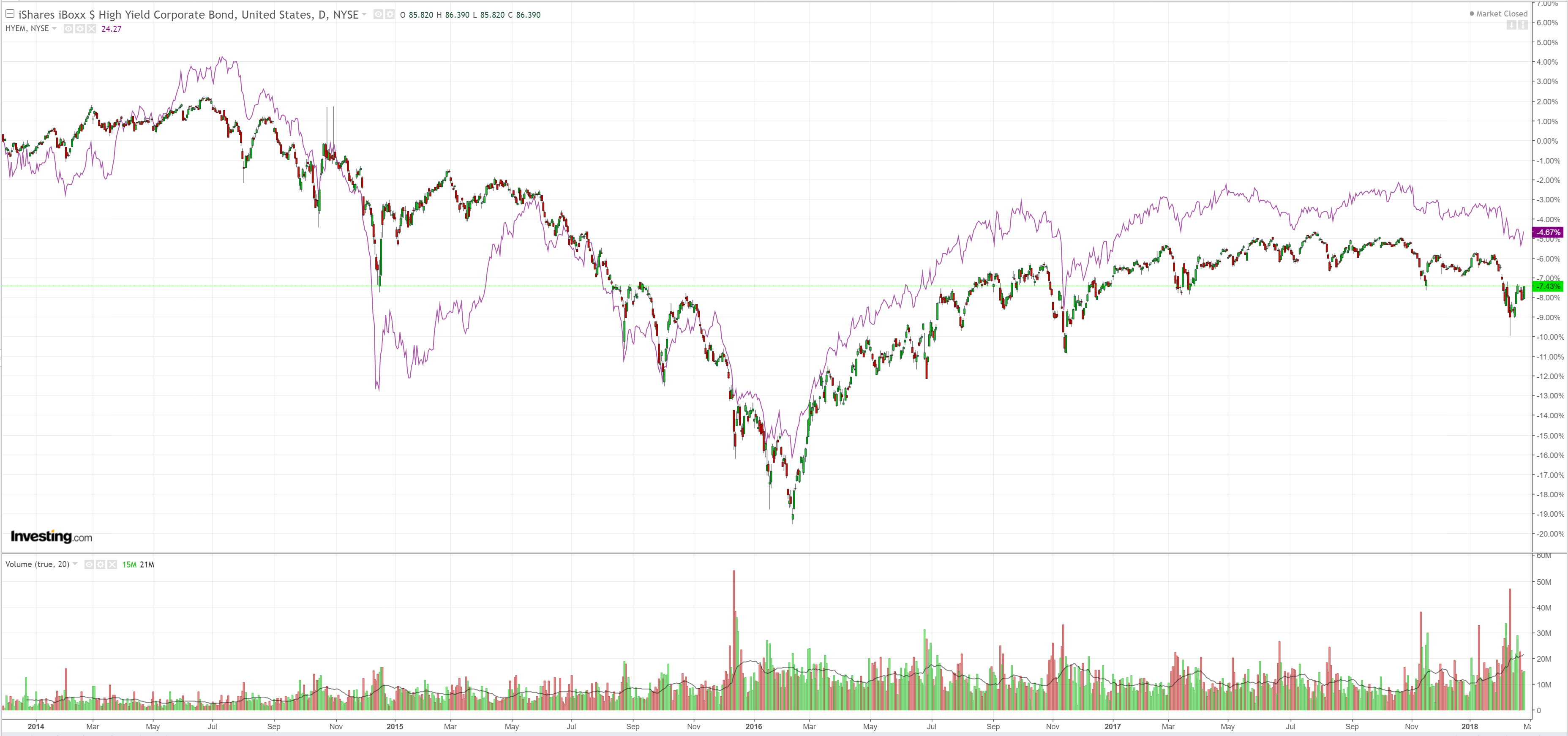

So did junk:

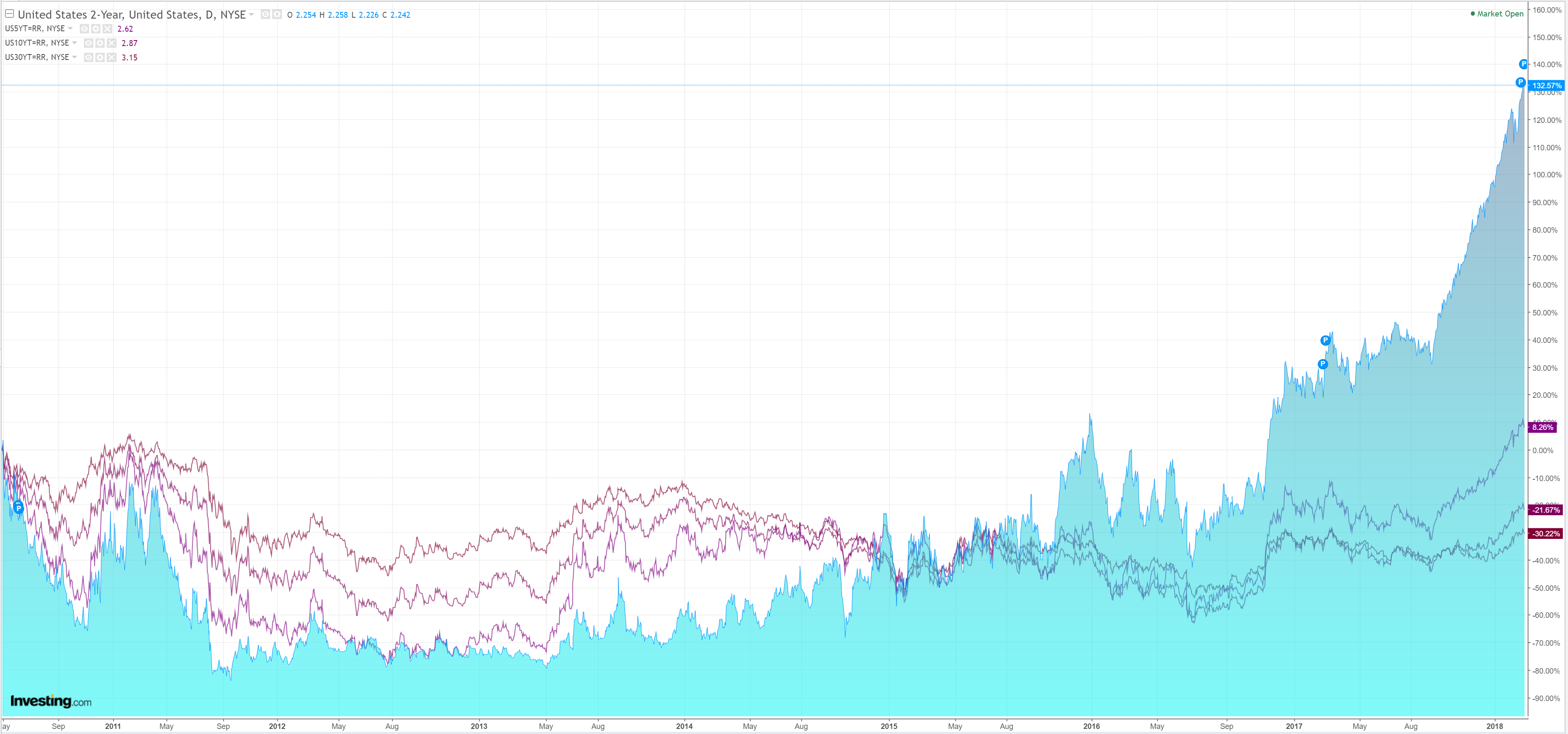

The key was a strong bid for Treasuries across the curve:

Advertisement

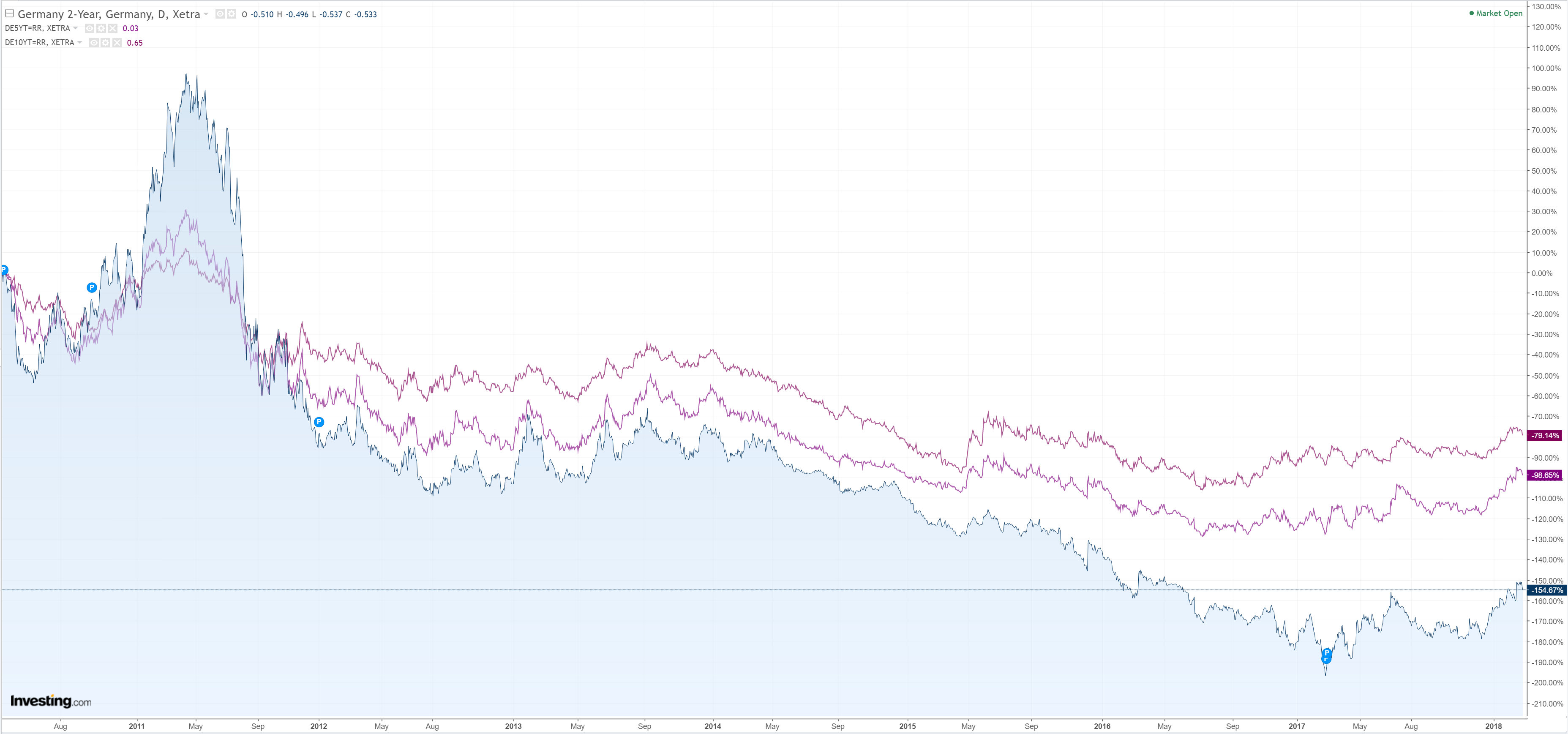

And Bunds:

Stocks took off to new post-correction highs:

Advertisement

There was not a lot to explain the bid in Treasuries that fired off the risk rally. China bailed out Anbang. European inflation was weak on target. Fed speakers were mixed.

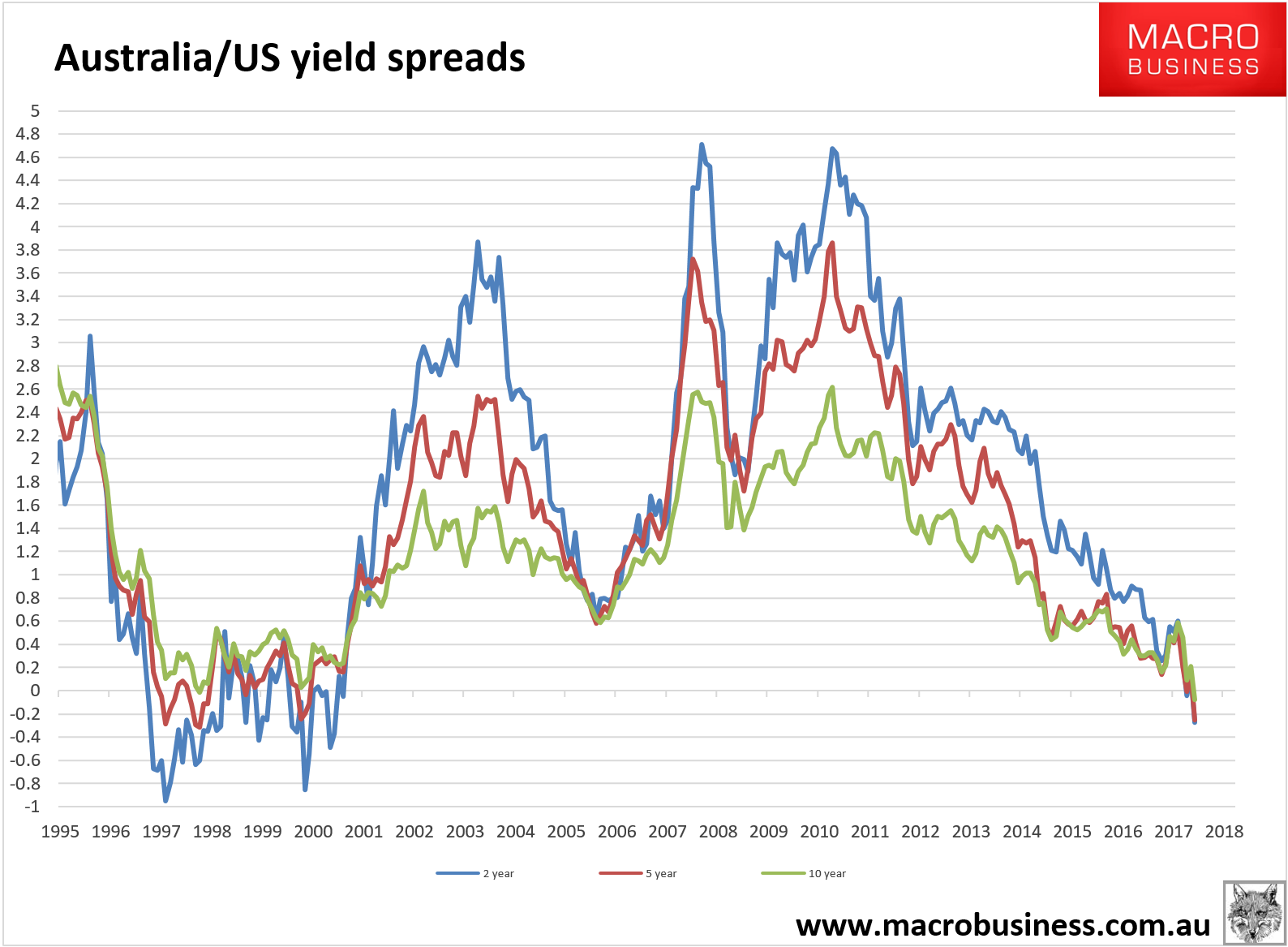

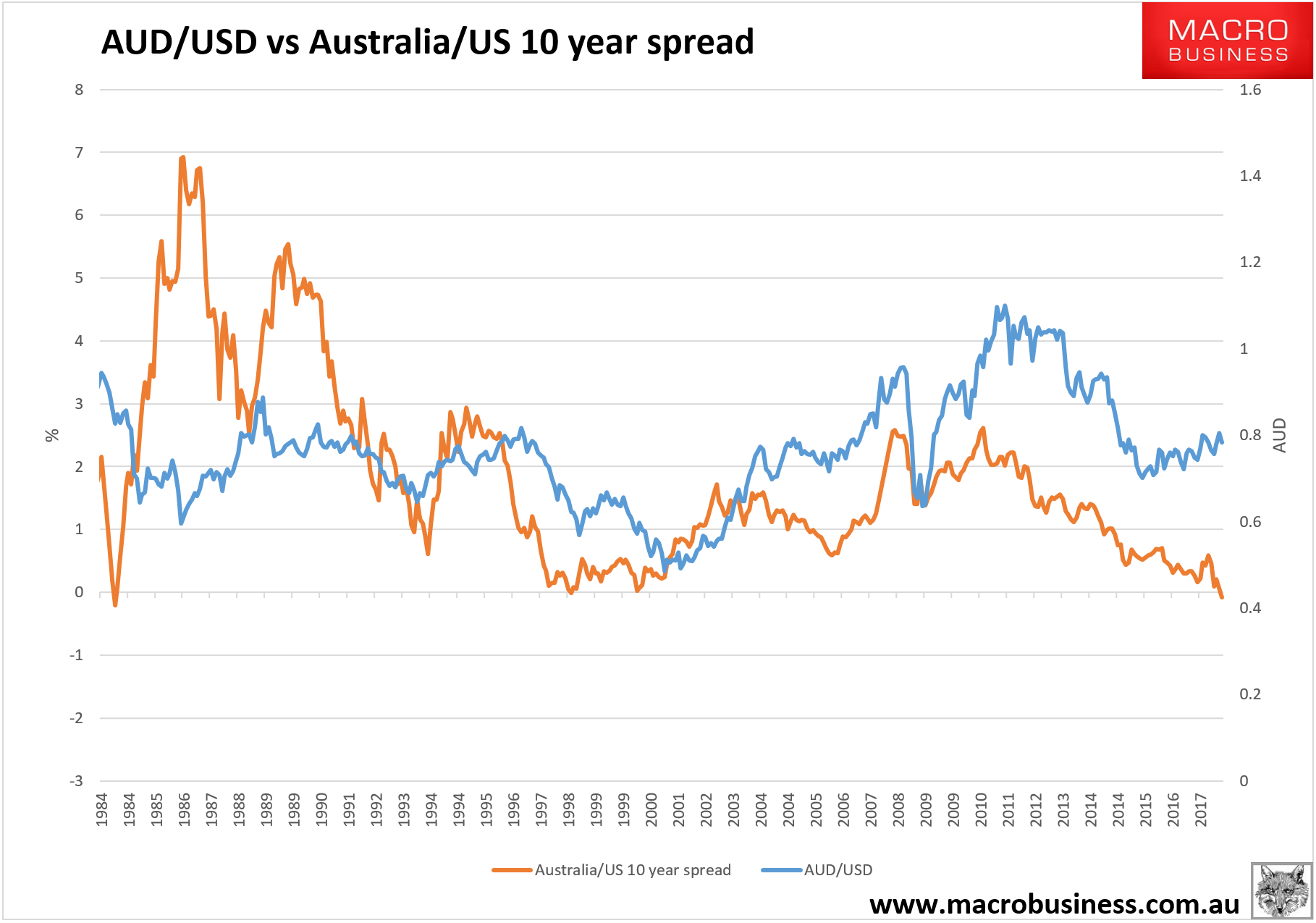

What was of note was the AUD weakness in the face of roaring risk on. It appears the rapidly deepening yield spreads are starting to impact the currency. All spreads hit new wides before pulling back a little. The 5 year breached -30bps, it’s deepest in eighteen years before retracing:

Advertisement

But remember how dislocated the currency is from the carry at the moment:

Higher stocks and a lower AUD puts the MB Fund in clover.

Advertisement

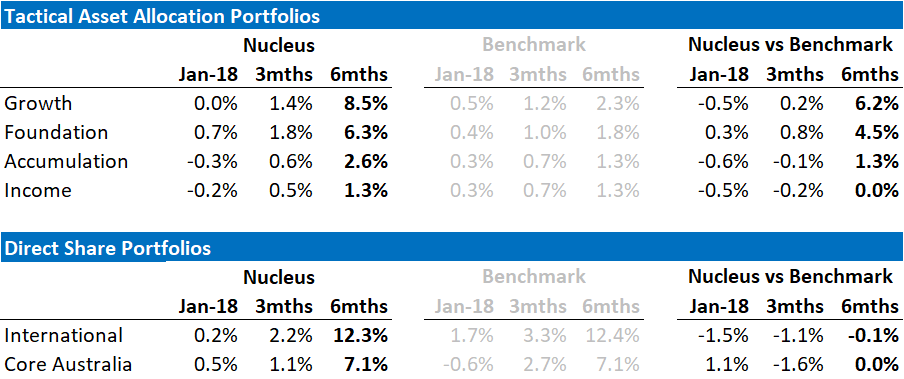

David Llewellyn-Smith is chief strategist at the MB Fund which is currently overweight international equities that will benefit from a weaker AUD so he definitely talking his book. Fund performance is below:

If these themes interest you then contact us below.

Advertisement

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.